The 'Gravity' of Stock Prices: Risk Free Rate

The 'Gravity' of Stock Prices: Risk Free Rate

The Unintuitive Relationship Between Stock Prices and Interest Rates

If you enjoy or get value from Investing Lessons, consider helping me reach 1,000 subscribers by the end of June (my birthday!) by doing any of the following:

Forwarding this post to friends, and getting them to subscribe.

Sharing on Twitter, Facebook, and Linkedin with a note of what you learned.

Sharing within community or company Discord/Slack/Facebook groups.

With the recent drop in stock prices, it is important for me to begin this week’s edition with a public service announcement. While it is normal to feel a sense of fear and anxiety when the market corrects, companies that were viewed as great long-term investments do not all of a sudden become bad investments purely due to the price going down.

When our favourite snacks go on discount at the local supermarket, it would be quite odd for one to panic. Rather, most would cherish this opportunity to buy more snacks at a discount. In a similar vein, we should embrace short term price fluctuations as an opportunity to build up a sizable position in high conviction names. It is also a time for us to reflect on how we are investing - is it through rational thought, or from greedy exuberance? [1]

Case Study

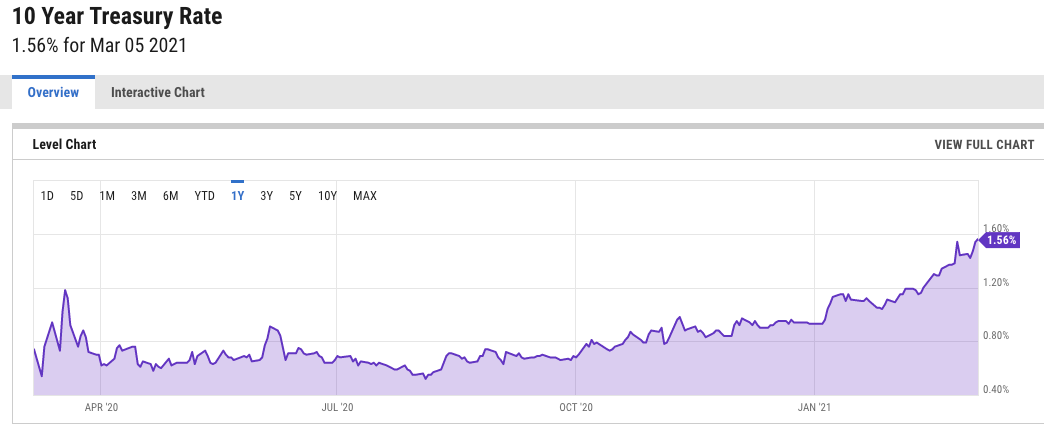

The recent rise in the 10 Year T-Bill rate was responsible for the multi-week decline in equity prices. For reference, a move greater than 5bps (0.05%) is considered large in the rates market.

Risk Free Rates: The ‘Gravity’ of Finance

Several months ago, you might have heard the narrative of people being confused by the markets reaching new highs amidst a worsening global pandemic. There were many growth companies that reached stratospheric prices, trading at extremely high valuations. With the recent decline in equity prices, it might be then easy to attribute this to stocks being overvalued. [2]

Here is a secret that is hiding in plain sight.

Everything in the market is valued against the ‘risk-free rate’ - this is typically the 10 Year U.S. Treasury Bill Rate. Just like what the name implies, the risk-free rate offers ‘guaranteed returns’, rooted in the assumption that the U.S. government has a zero risk of defaulting on loans. It is worth noting the lengthy list of nations that have defaulted in the past.

For those unfamiliar with treasury bills or bonds, it is effectively a mortgage - but in reverse. When you purchase a 10 year T-bill with a 1.50% yield, the government effectively has taken out a loan from you. Not only do they need to repay the initial loaned principal, but they pay you 1.50% in almost-guaranteed interest every year. More on bonds in future editions.

Whenever you decide to purchase any investment, you are implicitly forgoing a guaranteed return in the U.S. 10-Year T-Bill for a potentially higher return in something riskier. To make sense of this statement, let us consider the following two extreme scenarios.

In scenario 1, let us consider a 10-year risk-free rate of 6%. If you had to choose between a bond and a high-growth company that is yet to be profitable, what would you pick? It is quite apparent that you would probably opt out to buy the bond as you are guaranteed to make 6% - which is a lot of money. This is exactly what precipitated the 2000 Dot-Com Bubble - investors sold equities for bonds, thereby crashing equity prices.

In scenario 2, let us consider the exact situation but with a risk-free rate of 0%. What would you do? All of a sudden bonds become extremely unattractive as not only do you receive zero interest, but there is no option for future upside in value. On the flip-side a high-growth company has the potential or option to be more valuable in the future, and it is able to grow more aggressively thanks to cheaper loans. This is our current market, which heavily favours equities.

In conclusion, decreasing rates generally increases equity prices, and vice versa.

Market Commentary

Here is a succinct summary of what happened in the markets in the last few weeks. Initially, the market operated on the assumption that the Federal Reserve (Fed) would keep rates low. The Fed is able to manipulate interest rates in order to maintain the stability of the financial markets.

Originally it was thought that the financial system will experience practically zero interest rates within five years. However with the endless amounts of stimulus issued by the government and a stronger than expected employment rate, inflation is running hotter than the desired Fed target range of 1.7 - 2.0%. [3] [4]

This led traders to believe that the Fed would raise rates in order to reduce inflation, despite Powell stating that he is fine with the high inflation level. This resulted in increasing 10-Year T-Bill Rates, thereby causing equities to fall.

Footnotes

[1] If you are significantly leveraged, this is definitely not a great time for that.

[2] Low interest rates favour high-growth stocks the most. As rates increase, there typically is a large rotation from high-growth tech stocks into more stable, inflation-resilient sectors such as financials or commodities.

[3] Yes, equities fell on better than expected employment levels - something that is usually viewed as a positive event. An increase in jobs means more recovery, which increases the velocity of money (that is currently low due to lockdowns), which increases inflation - meaning that the Fed is more likely to hike rates.

[4] My personal hypothesis is that the Fed actually do not want to increase rates just yet. It is likely that they want inflation to run up to 3%, so that they are able to increase rates successively to 1.5-2% (while reducing inflation back to the 1.7-2% target range). This will give them extra dry-powder again if another recession occurs. If they hike rates prematurely, then they might not be able to hike rates high enough.