Is Bitcoin Worth $1,000,000?

Is Bitcoin Worth $1,000,000?

Bitcoin Investment Thesis from First Principles

If you enjoy or get value from Investing Lessons, consider helping me reach 1,000 subscribers by the end of June (my birthday!) by doing any of the following:

Forwarding this post to friends, and getting them to subscribe.

Sharing on Twitter, Facebook, and Linkedin with a note of what you learned.

Sharing within community or company Discord/Slack/Facebook groups.

Cryptocurrencies have once again entered the public spotlight, following Bitcoin’s recent surge to USD $40,000. Having begun my career trading cryptocurrency derivatives on Wall Street, I naturally am intrigued by crypto-assets as an investment.

Like many, I had always been a skeptic - despite having built quant algorithms to trade Bitcoin. Upon every attempt to uncover objectivity, I am always met with the irrationality of Bitcoin cult followers, sensationalist media or the FOMO of retail traders.

The lack of a first principles investment thesis for Bitcoin is concerning. Without conviction, we are at mercy to our own emotions during Bitcoin’s volatility. It is only when you are confident in your strategy that you can stomach large downturns, and be greedy when others are fearful. Even if you bought at the peak of Bitcoin Mania in 2018, you would still have returned 100% within 3 years had you not sold.

Today I present not from a trader’s perspective, but that of a rational long-term investor. This is not a get-rich-quick technical trading tutorial - they are a fugayzi, fake. I hope this will help you make a better informed decision with respect to incorporating Bitcoin into your portfolio.

Two Major Functions of Cryptocurrencies

A quick search will reveal a plethora of over a thousand different cryptocurrency coins. These include the most popular cryptocurrency, Bitcoin, and also other ‘alt coins’ such as Ethereum, Litecoin, and Dogecoin. While it may be overwhelming to understand what each crypto token does, there are two main use cases - (1) as a utility protocol, or (2) as a store of value.

Utility protocol tokens exist to distribute limited network resources, allowing users to gain access to features such as smart contracts or payment systems. In order to maintain such a system (also known as the blockchain), it has real world costs in the form of computational power. These tokens are rewarded to the ‘miners’ that maintain the blockchain.

Due to Bitcoin and several other alt coins being finite in supply and robust from hacking, there are arguments made for it to become a potential non-fiat store-of-value asset like gold. What makes cryptocurrencies potentially more special than gold is that it can be also non-sovereign, meaning it is not associated with any country. Commodities like gold are generally sold in USD denominations, thereby giving America too much control over the currency markets.

I will make the case that the only compelling reason to invest in Bitcoin is its potential to emerge as the dominant non-sovereign non-fiat store-of-value. The valuation for it to be a utility protocol is by definition limited, as the purpose of the blockchain is for fast, cheap transactions at scale. It is also likely for the utility protocol market to be fragmented across several crypto tokens, each serving its own niche market segment - just look at how many payment options there are today.

Part 1 - The Value of Cryptocurrency as Utility Protocol Tokens

For any given cryptocurrency protocol, it can be seen as a simplified economy - where utilities can be traded for tokens that are worth some monetary value. At maturity, these tokens do no more than allocate computational resources efficiently.

The Value of Utility Tokens is Tied to its Underlying Costs

The maturity of cryptocurrencies is a reasonable proxy for economic equilibrium, where marginal utility equals to the marginal cost. This means that the value of these cryptocurrency tokens cannot materially decouple from the underlying cost of resources.

If you are still not convinced, let us imagine the following thought experiment. Suppose we have a blockchain that is expensive to use. One of two likely scenarios will occur. In scenario one, competition between miners will occur, as they undercut one another to claim more reward tokens, thereby decreasing the cost. In scenario two, users will create a forked blockchain. This is an identical network, but with a lowered cost. These two scenarios will occur until there are no further arbitrage incentives.

Valuing the ‘Market Cap’ of Utility Tokens

Earlier we alluded that cryptocurrencies are effectively its own micro-economy. The GDP or ‘market cap’ of such an economy can be explained with monetary economics theory.

The money supply or ‘market cap’, M, is simply a function of the aggregate cost of computational resources needed to maintain the blockchain (PQ) divided by the velocity (V) in which the crypto token is being used.

M = PQ/V

where:

PQ = the total cost of computational resources consumed (price * quantity)

V = the average frequency with which a token is used (velocity)

In the long run, the cost of computational resources (P) is deflationary due to Wright’s Law. Furthermore, we are currently far from the theoretical upper limit of velocity (V), as circulating tokens can potentially wizz around at the speed of computational processing.

These trends ultimately reduce the ‘market cap’ (or M) of a particular utility protocol in the long run. In plain English this means that blockchain technology is bullish for its users, capable of delivering fast, robust, cheap utility services such as payments at scale - it is however bearish for investors in utility tokens. In fact Ethereum’s in-built Gas protocol aims to ensure this.

The King of Utility Protocol Tokens (Ethereum) as an Investment

The current leading utility protocol token is Ethereum, with many dApps and protocols built on the Ethereum network. As an investor, it is therefore reasonable to begin an analysis in utility protocols by first valuing Ethereum. All quantitative calculations are located here.

At the day of posting, the daily cost of transactions on the Ethereum network totals about 2400 Ethereum tokens, or about USD $3 million per day. If we make the assumption that the Ethereum network grows 1.5x YoY and the cost of resources decreases by 20% YoY - the ‘market cap’ of Ethereum effectively doubles every year.

Assuming that the velocity of Ethereum is 7, equal to that of the US dollar, then the 10-year projection of total Ethereum is expected to be USD $200 billion. The current total value of Ethereum is USD $158 billion, giving it a mere 26% upside over 10 years. This is simply insufficient return for a speculative asset with inherent long-term deflationary forces.

Part 2 - The Value of Cryptocurrency as Money

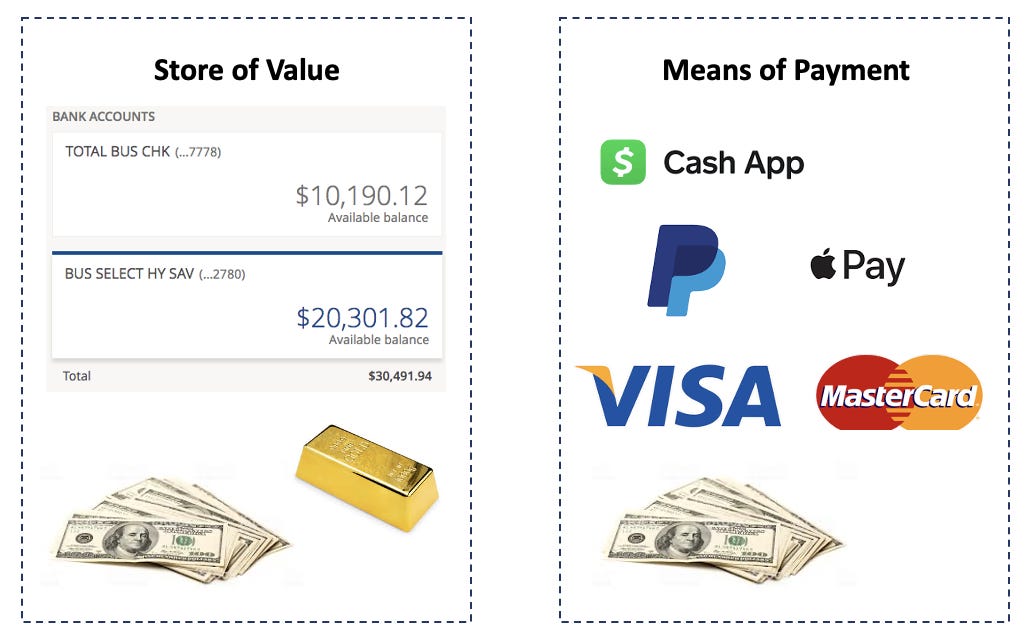

Money in a sense, is simply a large debt ledger or excel table. It was invented so that we longer need to barter for specific goods, as money acts as a unit of account for goods or services to be compared against. Money can either act as a store-of-value (e.g. gold and physical cash), or it can be a means of payment (Visa, Paypal, Apple Pay, Cash App, physical cash).

An interesting observation here is that traditionally, only physical cash has been able to act as both a store-of-value and a means of payment. We certainly cannot store value on a credit card, nor can we purchase dinner with a lump of gold.

The Potential for Cryptocurrency as Money

One way to gauge the potential for cryptocurrency as money is to compare it against existing technologies. On a preliminary glance, it appears that cryptocurrencies also have the potential to serve this dual function.

It can be argued that cryptocurrencies is a better store-of-value than physical cash, given that it can never be diluted unlike fiat currencies at a whim. Furthermore it is secure and practically unhackable - if this was not true, Bitcoin would devalue rapidly. As it is not a physical commodity, it poses minimal storage costs (or cost of carry) unlike gold.

As a means of payment, cryptocurrencies are currently lacking in day-to-day transaction functionalities compared to Apple Pay or Google Pay. Nonetheless, they have superiority in certain niche use cases such as with international payments.

Due to the recent support for Bitcoin on popular fintech platforms such as Square’s Cash App or Paypal’s Venmo, the layer of payment frictions is rapidly reducing. This support for Bitcoin serves to evangelise it, acting as a powerful marketing instrument for wider adoption.

The value of a cryptocurrency is effectively derived from its value as a means of payment plus its value as a store-of-value. As payments is simply a special case example of a utility protocol, we have discussed at lengths previously that there is limited value here.

Rather the bulk of a cryptocurrency’s valuation, is its potential to emerge as a dominant non-sovereign non-fiat store-of-value.

The Case for Bitcoin as the Dominant Store-of-Value

An asset is described to be a store-of-value when it is decoupled from the cost of manufacturing and storing it, or its functional utility. Gold is an example of a store-of-value, as it is arbitrarily expensive relative to its utility - most gold is kept as giant inert bullions for no other purpose.

Given Bitcoin is the most popular cryptocurrency with extremely robust features, it is the leading candidate to be the dominant store-of-value. While it can be argued that there may be more than one crypto-assets that can serve this purpose, there is also no real utility in having multiple candidates. We simply just need to look at silver, which is a fraction of the value for gold.

A logical place to start estimating the value for Bitcoin if it successfully becomes the dominant non-fiat store-of-value, is to look at the current standard - gold bullions. Currently there is c.198,000 metric tonnes of gold above ground, valued at USD $11.6 trillion. About 39% of these (USD $4.5 trillion) are held in bullions, split among the private sector and national treasuries.

The value of Bitcoin in 10 years will be some multiple (or fraction) of the total value of gold bullions today. Given that we expect governments to be more prudent, a bearish case in valuation can be 0.25x for national treasuries and 0.75x for the private sector. Similarly, a bullish case might see valuations of 1x for national treasuries and 3x for the private sector.

This gives Bitcoin a value of between USD $130,000 - $530,000 if it is successful in becoming the dominant non-fiat store-of-value. Assigning multiples is the most subjective element of this analysis, and all underlying assumptions are found here.

It should be caveated that having a tremendous upside does not make Bitcoin a good investment, more on this will be covered later in the article. The downside of unsuccessful adoption is effectively a 100% loss. However, a more bullish case may be possible if Bitcoin is widely used to replace unstable sovereign currencies, such as the Venezuelan bolivar.

The Case for Bitcoin to be Part of the International Reserves

Displacing gold bullion may just be the tip of the iceberg, as there is also the potential for Bitcoin to become integrated into the international reserves. There it will act as a non-sovereign, non-fiat, store-of-value asset, or country agnostic.

Currently gold represents about 11% of the USD $12 trillion in total international reserves. The remainder 89% is held as a basket of international fiat currencies, with a large proportion of it held in USD. The disproportionate amount in USD holdings is a result of all major commodities being priced in USD denominations, and America being a significant player in global trades.

With recent trade wars and ongoing economic tensions between countries such as China and the United States, it is not an ideal situation to hold the majority of its reserves in USD. Reducing the amount of USD in international reserves reduces the amount of control America has over countries.

This makes a case for a potential non-sovereign, non-fiat, store-of-value asset like Bitcoin compelling. In the instance that Bitcoin is able to replace 10% - 75% of fiat-currency international reserves, this adds an additional USD $60,000 - $440,000 to the value of Bitcoin.

Adding both scenarios up, if Bitcoin is successful in becoming a non-sovereign, non-fiat, store-of-value asset, its potential valuation in 10 years will be USD $191,000 - $970,000.

Part 3 - Determing if Bitcoin is a Rational Investment

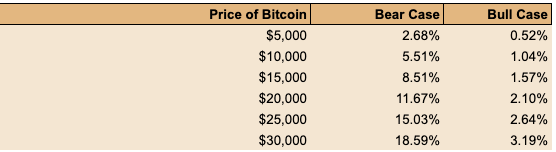

An important aspect of determining if Bitcoin is a rational investment, is to see if it is a positive expected value bet. At my most recent entry point, Bitcoin was valued at USD $10,000. Given the valuation projections made above, I only needed to be right about 1 - 5% of the time to break even in the bull and bear scenarios respectively.

Given the increased adoption of Bitcoin by major fintech players (Venmo and Cash App) and hedge funds, I think reasonably there is a greater than 5% chance of it succeeding. This not only makes it a positive expected value bet, but one with an asymmetric payoff skew of -1x to 100x. This is akin to purchasing a lottery ticket, that earns you money on average.

At currency valuations of USD $30,000, you need to be right 3% in the bull case and 19% in the bear case. If you think that the odds of Bitcoin successfully becoming a non-sovereign, non-fiat, store-of-value asset within the next 10 years is greater than that, you should invest in Bitcoin.

If you have accepted that Bitcoin’s net expected value is positive for the current price, then you should enter a position. However given that Bitcoin is an extremely speculative asset, then the best way to manage risk is through bet sizing. It should occupy a small proportion of your portfolio (1 - 5%), and it certainly shouldn’t be bought on margin. For a more technical breakdown on how traders or poker players manage bet sizing, read up on Kelly Criterion.

As a concluding note, if any of the fundamental assumptions change, then you need to update your investment thesis in a similar fashion. Happy investing.