Beginner's Guide to Market Making (with examples)

Beginner's Guide to Market Making (with examples)

Anyone could be a market maker

If you enjoy or get value from Investing Lessons, consider helping me reach 1,000 subscribers by the end of June (my birthday!) by doing any of the following:

Forwarding this post to friends, and getting them to subscribe.

Sharing on Twitter, Facebook, and Linkedin with a note of what you learned.

Sharing within community or company Discord/Slack/Facebook groups.

Previously, we discussed how market makers function as middlemen in exchanges, acting as both a willing buyer and seller. These offer a variety of benefits such as improved liquidity, greater market resilience, thereby saving investors $3.6B in trade execution fees in 2020.

Today, I will walk through some basic concepts of market making with real examples. These are the foundations of all automated high-frequency strategies run at firms like Jane Street, Optiver, Susquehanna, Citadel, and IMC. Here is a link to the raw data if you want to follow along.

In non-liquid markets such as cryptocurrencies back in 2016, these were exploitable by retail traders without the need of low-latency bots. Another interesting market to exploit this is in-game economies for video games like Runescape - a game where I spent thousands of hours on, that helped develop my intuition of finance.

1. Arbitrage

Law Of One Price

An arbitrage is the simultaneous buying and selling of identical assets in different markets to profit off discrepancies in the listed price. This is grounded in the law of one price, an economic principle that states that the price of an identical asset will have the same price everywhere.

Suppose we have Andrew selling apples for $1 each on the continent of Australia. His neighbour Bill in New Zealand simultaneously wishes to buy apples for $2 each. An arbitrage here would be simply being smart enough to recognise that an apple should have one price, and that you can make money by buying low and selling high!

However in the real world such opportunities rarely exist because once someone catches wind of it, they will exploit it. Once everyone is doing it, then these price discrepancies will slowly disappear - this phenomenon is called the market becoming more efficient. Classic examples of this includes dropshipping, or flipping items.

Another often overlooked factor is fees. In the example above, what would happen if it costs the market maker a $1000 plane ticket in order to deliver the apples from Andrew to Bill? Rather than profiting $10 from this sneaky transaction, you would be down $990 instead.

Trading Case Study

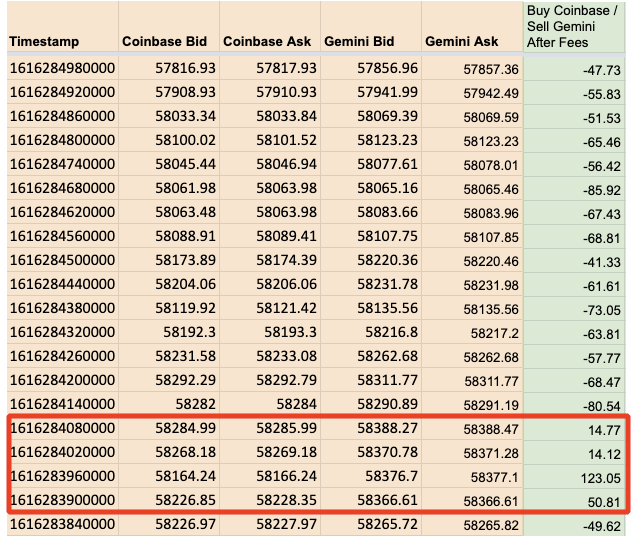

Below is a real case study to illustrate the concept in live action. We have two exchanges Coinbase and Gemini, each quoting Bitcoin (BTC) in USD - both with 0.075% market taking fee.

Recap: The bid is the price that you can instantly sell at, whereas the ask is the price that you can instantly buy at on the exchange. Whenever you are ‘crossing the spread’ to buy/sell from the ask/bid respectively, you are market taking from someone that is market making.

On first glance, there seems to be an obvious arbitrage in the first row. You could buy BTC on Coinbase for $57,817.93 and sell BTC on Gemini at $57,856.96 - banking in $39.03 profit.

Sometimes price discrepancies cannot be exploited. It should be pointed out that you need to pay the exchange 0.075% taking fee whenever you cross the spread. This is a percentage of the notional value of Bitcoin that you are transacting at - e.g. 0.075% * $57,817.93 = $43.36. Paying for both legs will book you a loss of $47.73.

However as illustrated by the red box in the image, there are times where arbitrage opportunities arise and an easy profit can be made. Generally as a rule, the more efficient an exchange is, the less arbitrage opportunities will present itself - as HFT firms with nanosecond-fast low-latency trade execution bots will have exploited it.

2. Market Making

Being Delta-Neutral

Market making in a nutshell is acting as a sports bookmaker, where you pair off punters against one another. In an ideal world, you don’t want to be long nor short a particular asset - also known as being delta neutral. You would be surprised to know that almost every market maker on Wall Street (with some few examples) run books that are close to delta neutral.

Terminology: The term delta arises from one of the option greeks, which simply refer to the rate of change in an asset’s price, if the underlying asset price changes by $1. For regular non-derivative assets like a stock, delta simply refers to the net position of the particular asset.

Being non-delta neutral is extremely risky, as you are now effectively punting directionally as to where the stock might go. There have been plenty of academic studies discussing how much alpha hedge funds have in stock picking.

In fact Renaissance Technologies are only right around 51% of the time when directionally stock picking - the legendary hedge fund that achieved 66.1% average annual returns since 1988.

Note that market making has subtle differences from a pure arbitrage, despite both being laughably ‘buy low sell high’. An arbitrage is riskless as both trades occur simultaneously. Market making is different to an arbitrage as buying and selling occurs passively at different times, during which the market can adversely move against you.

Having Bullets To Quickly Unwind Risk

When market making, there is a concept called bullets - options you have at your disposal to quickly unwind out of different risks.

For instance, if you had been quoting BTC and you got lifted on your ask (someone bought from your asking price), you are now short a Bitcoin. Suppose you did this by accident, then a bullet you have at your disposal is to simply buy back a Bitcoin.

While this example might seem trivial, finding liquidity in times of dire need is extremely expensive, if not impossible. A classic example is during scenarios such as a short squeeze.

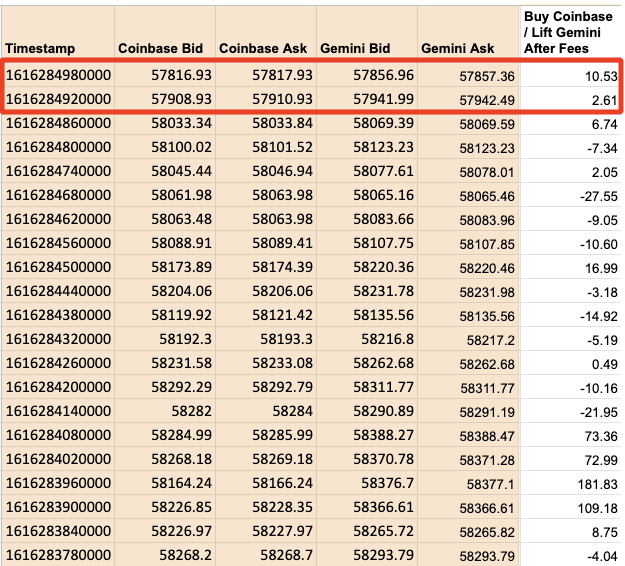

If we return to look at the case study above, it can be noted that sometimes unwinding out of risk can still be profitable. In the first row, let us suppose you got your ask lifted on Gemini, thereby selling BTC at $57,857.36 - you are now short one BTC. Suppose you then wanted to return to being delta neutral, you could purchase a BTC on Coinbase for $57,817.93.

Suppose you received a 0.025% rebate for market making on the Gemini leg, and paid a 0.075% fee for taking on Coinbase - you would be up $10.53.

While this is certainly a profitable trade, there is no good reason to cross the spread and unwind out of your risk unlessabsolutely necessary. You are leaving money on the table by paying a $43 fee, when instead you probably could have waited patiently to get lifted on the bid in order to return to a flat position.

Leaning On Your Bid-Ask Quote

The reason why crossing the spread to unwind out of your risk is generally unnecessary, is because as a market maker, you have another bullet at your disposal - the spread.

Suppose you are a market making an apple, which has a permanent fair value of $2 each. You as the market maker would generally quote a bid-ask that is symmetrical, such as $1 - $3 (Your bid is $1 and your ask is $3).

Throughout the day, you realise that people having been aggressively hitting your bid, resulting in you accruing a long position of apples. Given that the fair value of an apple is still $2, then one way to be buying less and selling more is to lean your position.

The concept of leaning is simply to widen out the side you want to quote less of, and tighten out the side you want to quote more of. Given that there is more demand on the bid-side, one can reasonably assume that widening out the bid to $0.50 will reduce the amount of apples sold to you. Conversely, tightening on the ask-side will increase demand. If we simultaneously tighten the ask to $2.50, you can expect to sell apples until your position is flat.

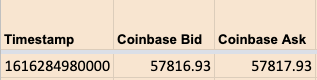

Suppose the current bid-ask spread for Bitcoin is as shown below. In order to more aggressively sell Bitcoin, you could improve the existing ask by quoting $57,817.50 (sometimes called price discovery).

For retail traders or investors, quoting a bid/ask inside the spread is probably the easiest way to reduce your cost basis - you are technically now market making!